+91-161-2301394

+91-161-2301394  Email US

Email US

[vc_row][vc_column][vc_column_text]

INTRODUCTIONFinance Act, 2020 brought about various changes in the provisions of Income Tax Act, 1961. One such change was the introduction of a new sub-section (1H) to section 206C. A step claimed to be taken by the Indian Government to curb and track unaccounted money and further to widen and deepen the tax base. The main emphasis of the current Indian Government is on voluntary compliances by the taxpayers and by this, department wishes to keep an eye on large number of taxpayers. The newly incorporated section requires the seller to collect from the buyer a sum equal to 0.1% of the sale consideration exceeding rupees Fifty Lakhs as income tax. As simple as that sounds, it comes with a lot of complications, which we have tried to resolve through this document.

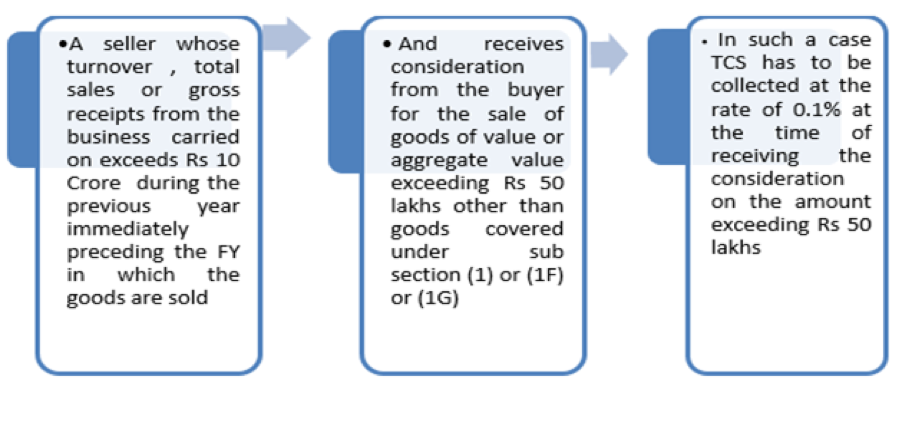

Understanding The Provisions Of The Newly Incorporated Section

The section requires every Seller, who receives any amount as consideration for sale of any goods of the value or aggregate of such value exceeding fifty lakh rupees in any previous year, to collect a TCS at the rate of 0.1% at the time of receipt of sales consideration exceeding rupees fifty lakhs, provided his total sales, gross receipts or turnover exceeds rupees ten crores in the immediately preceding financial year, in which the sales of goods is carried out.

[/vc_column_text][/vc_column][/vc_row][vc_row][vc_column][vc_tta_accordion style=”outline” color=”green” active_section=”1″][vc_tta_section title=”Exclusions” tab_id=”1601626462696-69853207-4b53″][vc_column_text]This section shall be not be applicable on the following:

Vis-à-vis Goods

(i) On goods Exported out of India;

(ii) On the goods covered under sub section 206C (1), 206C (1F) and 206C (1G) on which specific rates have already been prescribed. Goods that are covered under various sub sections on which this section is not applicable can be summarized below:

| Section | Nature of Goods Sold |

| 206C (1) |

Alcoholic liquor for human consumption Tendu leaves Timber obtained under a forest lease Timber obtained under any mode other than under a forest lease Any other forest produce not being timber or tendu leaves Scrap Minerals, being coal or lignite or iron ore. |

| 206C (1F) | Motor Vehicles (if value exceeds Rs 10 Lakhs) |

| 206C (1G) | Sum of money for remittance out of India (above Rupees Seven Lakhs) |

(iii) Also, sellers will not be liable to collect TCS, in case where the buyer of the said goods is liable to deduct TDS on those goods, under any provisions of this Act and has deducted such TDS. Therefore, if TDS is being deducted already by the buyer on such goods, no TCS shall be required to be collected by the Seller.

Vis-à-vis Buyer

The TCS shall be collected from all the buyers, except:

(i) the Central Government, a State Government, an embassy, a High Commission, legation, commission, consulate and the trade representation of a foreign State; or

(ii) a local authority as defined in the Explanation to clause (20) of section 10; or

(iii) a person importing goods into India or any other person as the Central Government may, by notification in the Official Gazette, specify for this purpose, subject to such conditions as may be specified therein;[/vc_column_text][/vc_tta_section][vc_tta_section title=”TCS in case of Non-PAN Buyers” tab_id=”1601626881079-585011d2-9e17″][vc_column_text]

The rate prescribed under this section is 0.1% on all goods, but the section further provides that if the buyer does not provide his PAN/ Aadhar number to the seller, the transactions will be subject to a higher rate of TCS of 1% instead of 0.1% in the former case.

[/vc_column_text][/vc_tta_section][vc_tta_section title=”Relief Amidst COVID” tab_id=”1601626936542-3163fc94-0172″][vc_column_text]

Further, in accordance with Press Release dated 13th May, 2020, wherein TDS and TCS were reduced by 25%, the amount of TCS required to be collected for payments to be received between 01.10.2020 till 31.03.2021 shall be restricted to 0.075%. However, no such relief has been given in case of Non-PAN buyers and TCS at the rate of 1% will be collected from such buyers.

[/vc_column_text][/vc_tta_section][vc_tta_section title=”Compliance” tab_id=”1601626990868-654fc8b0-0bdd”][vc_column_text]

Under this section, the liability to collect TCS arises, when the seller receives the sale consideration in excess of rupees fifty lakhs and the seller being the person responsible for collecting tax under the newly incorporated section shall deposit the TCS amount within 7 days from the last day of the month in which the sales consideration was received. Further, he shall also submit quarterly TCS return i.e., Form 27EQ in respect of the tax collected by him in a particular quarter.

Suppose if the Sales were made on 15th April, 2020 of Rs. 70 lakhs and the entire consideration is received on 15thOctober, 2020. In this case, the seller shall be required to deposit Rs. 1,500/- [(70,00,000 – 50,00,000) X 0.075%] upto 07th November, 2020.

[/vc_column_text][/vc_tta_section][vc_tta_section title=”Frequently Asked Questions (FAQ’s)” tab_id=”1601627063652-90e6e8bd-60de”][vc_column_text]

The section implicitly provides the point of collection of tax as the time of receipt of sales consideration. To understand it better, let us go through the following the illustrations:

[/vc_column_text][vc_toggle title=”Suppose Mr. A sold goods worth Rs. 60 lakhs during the period beginning from 01st April, 2020 till 30th September, 2020. An amount of Rs. 55 lakhs has already been received against such sale upto 30th September, 2020. The balance amount of Rs. 5 lakhs is received on or after 01st October, 2020. Whether TCS shall be required to be collected on the entire amount of receipt or only on the amount received on or after 01st October, 2020?” open=”true” css_animation=”bounceIn” custom_font_container=”tag:p|font_size:12|text_align:justify” custom_use_theme_fonts=”yes” use_custom_heading=”true”]It has been clarified by the department through its Circular No. 17/2020 dated 29th September, 2020 in point 4.4.2 of the said circular, that provisions of TCS shall not apply on sale consideration received before 01st October, 2020. Therefore, only the amount received on or after 01st October, 2020 shall be liable for collection of TCS i.e., Rs. 5 lakhs in the instant case.[/vc_toggle][vc_toggle title=”Q2: If during the current financial year i.e., 2020-21, the total sales made to a buyer does not exceed rupees fifty lakhs rupees. However, the total receipts from the said buyer in aggregate, including advances or consideration received in respect of opening balances is more than rupees fifty lakhs. Whether TCS is required to be collected in such case? If yes, then on what amount?” css_animation=”bounceIn” custom_font_container=”tag:p|font_size:12|text_align:justify” custom_use_theme_fonts=”yes” use_custom_heading=”true”]The liability for collection of TCS under section 206C(1H) has been cast upon the seller, when the seller receives sales consideration in excess of rupees fifty lakhs, in respect of sales of any goods of the value or aggregate of such value exceeding fifty lakh rupees in any previous year. Therefore, the TCS will be collected on the amount received from the buyer in excess of rupees fifty lakhs, irrespective of the year in which such sales were made or are to be made.[/vc_toggle][vc_toggle title=”Q3: Whether for calculation of the total threshold limit, the amount of indirect taxes, like GST shall be included?” css_animation=”bounceIn” custom_font_container=”tag:p|font_size:12|text_align:justify” custom_use_theme_fonts=”yes” use_custom_heading=”true”]

It has been clarified by the department through its Circular No. 17/2020 dated 29th September, 2020 in point 4.6 of the said circular that no adjustments with respect to GST is required to be made and even the section requires assessee to collect TCS on the amount of receipt from a buyer. Therefore, the entire receipts including GST, if in excess of rupees fifty lakhs, shall be liable to TCS.

Though as per our understanding, circular No. 23/2017 dated 19th July, 2017 clarified that TDS on GST is not required to be collected. However, under TCS regime, TCS is collected even on the GST amount, which is more or less a tax on tax. How good it holds in the court of law, will have to be seen in times to come.

[/vc_toggle][vc_toggle title=”Q4: Whether any adjustments in respect of discount given or sales return will have to be made for the purpose of collection of tax?” css_animation=”bounceIn” custom_font_container=”tag:p|font_size:12|text_align:justify” custom_use_theme_fonts=”yes” use_custom_heading=”true”]

It has been clarified by the department through its Circular No. 17/2020 dated 29th September, 2020 in point 4.6 of the said circular that no adjustments with respect to sales return or discount is required to be made. Section 206C(1H) requires assessee to collect TCS on the amount of sales consideration received from a buyer, if the consideration thereof is more than rupees fifty lakhs. Therefore, where the buyer has made the net payment thereof considering the sales returns or discounts, then the liability for collection of TCS shall arise only on the net amount. However, if the buyer has made the total payment and later on adjustments pertaining to sale return or discounts have been made, no adjustment/reversal of TCS will be made subsequently.

[/vc_toggle][vc_toggle title=”Q5: Whether any TCS will required to be collected in Year 2 or Year 3 in the following example ?” css_animation=”bounceIn” custom_font_container=”tag:p|font_size:12|text_align:justify” custom_use_theme_fonts=”yes” use_custom_heading=”true”]

| Particulars | Year 1 | Year 2 | Year 3 |

| Total Sales | 10.71 Crores | 9.57 Crores | 10.23 Crores |

| Sale of goods to M/s RJ Pvt. Ltd. | – | 70 Lakhs | 40 Lakhs |

| Amount Received | – | 10 Lakhs | 60 Lakhs |

The newly incorporated section casts twin condition for its applicability:

- The total sales, gross receipts or turnover from the business exceeds ten crore rupees during immediately preceding the financial year in which sale of goods is carried out; and

- The amount of consideration received in respect of sales of goods exceeds rupees fifty lakhs.

Therefore, the liability to collect and deposit TCS shall arise only when the twin conditions as envisaged above are satisfied.

In the instant case, the assessee will not be liable to collect TCS in Year 2 or Year 3 as both the conditions are not satisfied in the said years. Had the total sales of the assessee in Year 2 also exceeded rupees ten crores, then the TCS would have been collected in Year 3 on the receipts of ten lakh rupees.

[/vc_toggle][/vc_tta_section][vc_tta_section title=”Best Practices” tab_id=”1601628264114-bb8e5bdd-26e2″][vc_column_text]

Going forward, it will be very difficult to track the sales made to a person, track the receipt of such sales and track the collection of TCS thereof as in other sections of TCS, the liability to levy and collect TCS arise at the time of debit or receipt, whichever is earlier. However, under section 206C(1H), the seller is required to collect TCS only when the amount of sale consideration received exceeds rupees fifty lakhs from a single buyer.

Therefore, it becomes vital to track the payments to ensure necessary compliance of section 206C(1H). Various companies are willing to add the TCS on the sales bill itself. However, there is no legal backdrop to collect the TCS at the time of sale, and even otherwise if that be the case, an additional liability to deposit such TCS shall arise on the assessee from the point the sales are recorded in the books. Therefore, if still assessee wishes to levy TCS on the sale bill, it is advised to open a separate TCS control account and supplier TCS control account in order to account for those TCS liabilities which the assessee is not actually liable to collect and deposit under section 206C(1H), but still the same has been levied by the assessee on the sales invoice.

In such scenario the ideal approach for passing the journal entry can be understood as under:

M/s XYZ Ltd. Sold good to M/s RST Ltd. Worth Rs. 1.00 crores @18% GST on 01st October, 2020. The sales consideration is received on 15th December, 2020.

At the time of recording of Sale i.e., 01.10.2020

M/s RST Ltd. A/c Dr. 1,18,00,000/- (inclusive of GST)

To Sales 1,00,00,000/-

To GST payable a/c 18,00,000/-

And

M/s RST Ltd. (TCS Contra) A/c Dr. 5,100/- (68 lacs X 0.075%)

To TCS Payable (TCS Contra) A/c 5,100/-

At the time of receipt of such consideration i.e., 15.12.2020

Bank A/c Dr. 1,18,05,100/-

To M/s RST Ltd. A/c 1,18,00,000/-

To M/s RST Ltd. (TCS Contra) A/c 5,100/-

And

TCS Payable (TCS Contra) A/c Dr. 5,100/-

To TCS Payable 5,100/-

Now, the assessee shall be required to deposit the said TCS collected with the department on or before 07.01.2021.

[/vc_column_text][/vc_tta_section][/vc_tta_accordion][vc_column_text]

CONCLUSION

Though the vision of the department to ensure a larger tax base and to curb tax evasion by bringing in greater transparency is applauded, but it is yet apprehended that whether the government has overlooked the impact it might have on the cash flows, especially in times when the world is looking out for measures to prevent far-reaching effects of the recession. Amidst global recession and uncertainty caused by the pandemic, it is a bold move of the Indian government to not postpone the applicability of this section.

Further, to ensure regular tax compliance and at the same time maintain internal control within the organisation, necessary checks and balances will have to be applied.

The government has further tried to resolve some basic issues with its circular 17/2020 dated 29.09.2020 and a press release dated 30.09.2020, still there are a lot of ambiguities and questions which requires due resolution and clarification from the department going forward.

Referred Documents

Circular 17/2020 dated 29.09.2020

Press Release dated 30.09.2020

[/vc_column_text][/vc_column][/vc_row][vc_row][vc_column][vc_column_text]

For more details please feel free to contact us.

Disclaimer: This blog is intended as a service to clients and to provide clients with assistance in general. It has been prepared for general guidance on matters of interest only and does not constitute professional advice. No person should act upon the information contained in this without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, Ashwani & Associates, its members, employees and agents accept no liability, and disclaim all responsibility, for the consequences of any person acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.[/vc_column_text][/vc_column][/vc_row]